Copayments are various than coinsurance. Like any type of insurance plan, there are some expenses that may be partly covered, or not at all. You should be mindful of these expenses, which add to your total healthcare cost. Less apparent expenses may consist of services supplied by a physician or health center that is not part of your plan's network, plan limits for specific type of care, such as a specific number of check outs for physical therapy per benefit duration, along with non-prescription drugs. To assist you discover the ideal plan that fits your spending plan, appearance at both the apparent and less apparent costs you might expect to pay (What is an insurance premium).

If you have various levels to select from, select the highest deductible amount that you can conveniently pay in a fiscal year. Discover more about deductibles and how they affect your premium.. Price quote your total variety of in-network doctor's gos to you'll have in a year. Based best way to sell timeshare upon a plan's copayment, accumulate your total expense. If have prescription drug requirements, build up your month-to-month expense that won't be covered by the plan you are taking a look at. Even strategies with thorough drug protection might have a copayment. Figure in oral, vision and any other regular and required care for you and your family.

It's a little work, but looking at all expenditures, not simply the apparent ones, will help you find the strategy you can afford. It will likewise assist you set a budget plan. This type of understanding will assist you feel in control.

Group medical insurance strategies are developed to be more affordable for companies. Staff member premiums are generally less costly than those for a specific health insurance. Premiums are paid with pretax dollars, which help employees pay less in yearly taxes. Companies pay lower payroll taxes and can subtract their yearly contributions when calculating income taxes. Medical insurance assists services pay for health care costs for their staff members. When you pay a premium, insurer pay a portion of your medical costs, including for regular medical professional examinations or injuries and treatments for mishaps and long-term health problems. The amount and services that are covered differ by strategy.

Or, their plan may not cover any expenses until they have actually paid their deductible. Normally, the higher a staff member's month-to-month premium, the lower their deductible will be.

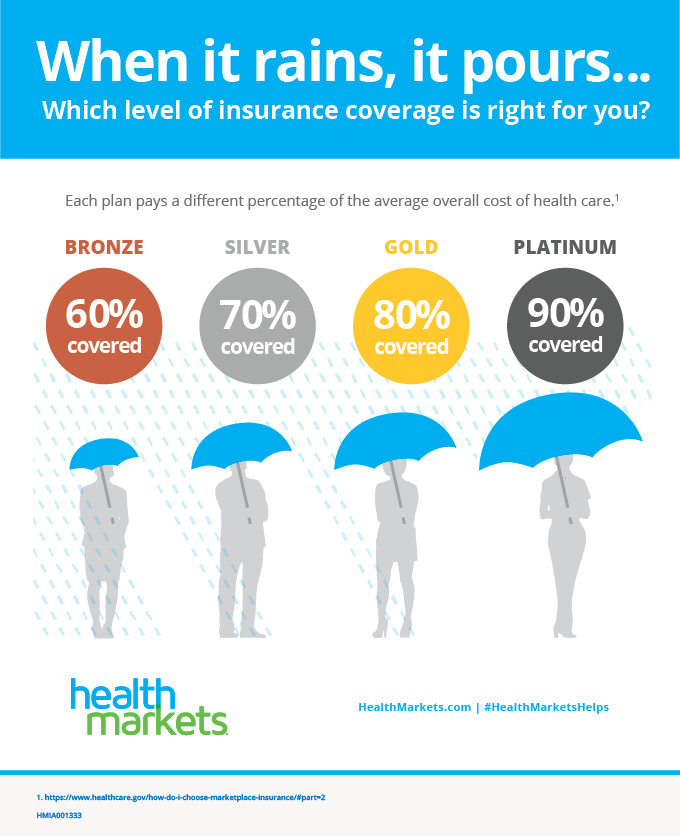

A deductible is the quantity you pay for healthcare services before your medical insurance begins to pay. A strategy with a high deductible, like our bronze strategies, will have a lower month-to-month premium. If you do not go to the physician often or take routine prescriptions, you will not pay much towards your deductible. However that could alter at any time. That's the threat you take. If you're hurt or get seriously ill, can you afford your strategy's deductible? Will you wind up paying more than you conserve?.

Related Topics How Are Deductibles Applied? The term "cost-sharing" refers to how health insurance costs are shared between companies and staff members. It is essential to comprehend that the cost-sharing structure can have a huge impact on the supreme expense to you, the company. Normally, costs are shared in two main methods: The employer pays a part of the premium and the remainder is subtracted from employees' paychecks. (Many insurers require companies to contribute a minimum of half of the premium cost for covered workers.) This might take the form of: copayments, a fixed quantity paid by the workers at the time they get services; co-insurance, a percent of the charge for services that is typically billed after services are received; and deductibles, a flat quantity that the staff members need to pay prior to they are qualified for any advantages.

Fascination About What Is Collision Insurance

With this in mind, the choices you'll have to make include: What quantity or percentage of the employee-only premium will you require the employees to cover? What quantity or percentage of the premium for dependents will you require the employees to cover? What level of out-of-pocket costs (copayments, co-insurance, deductibles, and so on) will your employees and their dependents sustain when they get care? Listed below we offer more info about premium contributions in addition to the different kinds of cost-sharing at the time of service: copayments, co-insurance, deductibles, and caps on out-of-pocket expenditures. A medical insurance premium is the total amount that needs to be paid in advance in order acquire coverage for a specific level of services.

Employers normally require staff members to share the cost of the strategy premium, usually through employee contributions right from their incomes. Bear in mind, nevertheless, that many insurance providers need the company to cover a minimum of half marriott timeshare presentation deals of the premium cost for staff members. Employers are complimentary to require staff members to cover some or all of the premium cost for dependents, such as a partner or kids. A copayment or "copay" as it is in some cases called, is a flat fee that the client pays at the time of service. After the patient pays the charge, the plan normally pays 100 percent of the balance on qualified services.

The fee normally ranges between $10 and $40. Copayments prevail in http://louisbgoz011.theglensecret.com/get-this-report-about-how-much-is-house-insurance HMO products and are often particular of PPO prepares too. Under HMOs, these services practically constantly need a copayment: This consists of sees to a network primary care or expert physician, mental health professional or therapist. Copays for emergency services are typically greater than for workplace visits. The copay is sometimes waived if the hospital admits the patient from the emergency clinic. If a client goes to a network pharmacy, the copayment for prescription drugs might range from $10 to $35 per prescription. Numerous insurance providers use a formulary to manage benefits paid by its strategy.

Generic drugs tend to cost less and are required by the FDA to be 95 percent as efficient as more expensive brand-name drugs marketed by pharmaceutical companies. To encourage physicians to utilize formulary drugs when recommending medication, a plan may pay higher advantages for generic or preferred brand-name drugs. Drugs not consisted of on the formulary (likewise called nonpreferred or nonformulary drugs) may be covered at a much higher copay or may not be covered at all. Pharmacists or medical professionals can recommend about the suitability of changing to generics. In numerous health insurance, clients must pay a part of the services they get.